Beirut Stock Exchange

Beirut, Lebanon · Established 1920

This site requires authorization to access.

To request access, contact

william.goetzmann@yale.edu

The Beirut Stock Exchange occupies quarters in the Azarieh Building, a landmark commercial complex in the Beirut Central District designed by the French architect André Leconte and completed in 1953. Leconte, who also designed Beirut International Airport at Khalde, produced a rationalist concrete-and-stone structure whose broad floor plates were intended to accommodate the commercial functions of a city consolidating its position as the financial entrepôt of the Middle East. The exchange’s trading hall was established under a 1920 decree of the French High Commissioner. The post-independence era of rapid banking expansion—the number of Lebanese banks grew from nine in 1945 to eighty-five by 1960, as Hicham Safieddine documents in Banking on the State: The Financial Foundations of Lebanon (Stanford University Press, 2019)—demanded modern facilities befitting Beirut’s ambitions. When the fifteen-year civil war devastated downtown Beirut, the exchange’s infrastructure was heavily damaged; trading halted entirely in 1983. Postwar rebirth came in stages: in 1994, a new administrating committee, established with the Bourse de Paris, overhauled internal bylaws. On November 22, 1996—Lebanese Independence Day—trading officially resumed in the refurbished hall. A 1999 cooperation agreement with the Bourse de Paris brought the NSC-UNIX Euronext continuous-trading electronic system, replacing open-outcry with screen-based execution. By 2002, the BSE had relocated to renovated quarters in the Azarieh Building within the Solidere-administered district transforming Beirut’s war-scarred center into what planners envisioned as a world-class business district. The catastrophic port explosion of August 4, 2020, causing an estimated $4.6 billion in destruction, once again tested the resilience of the district’s commercial infrastructure.

The decorative program of the Beirut Stock Exchange and its surrounding precinct reflects the layered aesthetic inheritance of a Mediterranean crossroads. The Azarieh Building’s modernist vocabulary—clean concrete surfaces, repetitive fenestration, functional floor plates—belongs to the rationalist tradition that André Leconte and contemporaries brought to mid-century Beirut, a style that architectural scholars have situated within a “Learning from Beirut” discourse linking European modernism to Levantine adaptation (George Arbid, ARCC Journal, 2002). The exchange sits within a district whose ornamental character is far richer. Along nearby Rue Maarad, arched stone facades inspired by the Rue de Rivoli line a boulevard radiating from the Place de l’Étoile, where the clock tower and Haussmannian elevations of the 1930s create a monumental ensemble that the Solidere master plan sought to preserve and extend. The postwar trading facilities prioritized technological transparency: the electronic floor fitted with the Euronext NSC system replaced open-outcry with rows of terminals—mirroring global trends toward minimalist, screen-mediated financial environments. Nevertheless, the broader Solidere reconstruction introduced elements referencing Beirut’s commercial heritage. Rafael Moneo’s Beirut Souks project (completed 2009), adjacent to the financial district, incorporated archaeological fragments—Phoenician commercial-quarter walls, Byzantine mosaics, a Mameluk madrassa—into a contemporary retail space deliberately echoing ancient cardo and decumanus marketplaces discovered beneath the site. The physical setting of financial activity in central Beirut is thus framed by an architectural palimpsest: Phoenician mercantile foundations, Roman colonnaded bazaars, Ottoman khans, French Mandate boulevards, and postwar glass towers all converge to shape the environment in which Lebanese capital markets operate.

Beirut’s position as the preeminent financial center of the Levant is inseparable from its urban geography—a compact promontory whose natural harbor connected Phoenician Berytus to Mediterranean trade networks three thousand years ago. By the mid-twentieth century the city had earned the sobriquets “Paris of the Middle East” and “Switzerland of the East,” reflecting both Francophone cosmopolitanism and bank-secrecy laws modeled on the Swiss example. Carolyn Gates, in The Merchant Republic of Lebanon: Rise of an Open Economy (I. B. Tauris, 1998), traces how dominant economic agents forged a laissez-faire model built on intermediary services and offshore finance, with Beirut’s central district as fulcrum. The Nejmeh Square–Rue Maarad area, planned during the French Mandate with radiating boulevards inspired by the Place de l’Étoile in Paris, concentrated parliament, banks, commodity traders, and the Bourse within walking distance of the port. When the civil war (1975–1990) bisected downtown along the Green Line, this commercial heart was gutted. Postwar reconstruction, entrusted to Solidere—the joint-stock company founded in 1994 under Prime Minister Rafik Hariri—became the most ambitious and controversial urban renewal in the modern Middle East. Saree Makdisi, in “Laying Claim to Beirut” (Critical Inquiry, vol. 23, no. 3, 1997), coined the term “Harirism” to describe the withering of public space and supremacy of private commercial interest. Samir Khalaf and Philip Khoury’s Recovering Beirut (E. J. Brill, 1993) similarly interrogated tensions between heritage preservation and speculative development. The August 2020 port explosion, damaging 77,000 apartments and 360 heritage buildings, reopened fundamental questions about the relationship between Beirut’s port and its financial core.

The Beirut Stock Exchange was established by decree of the French High Commissioner in 1920, making it the second-oldest organized securities market in the Arab world after the Egyptian Stock Exchange. Initially restricted to gold and foreign currencies, by the early 1930s the board expanded to company shares, with French, Syrian, and local Lebanese investment fueling listings of mixed Franco-Lebanese joint-stock companies quoted simultaneously in Paris and Beirut. The postwar boom transformed Lebanon into what Carolyn Gates termed a “merchant republic”—a small open economy whose laissez-faire credo attracted regional capital, especially after nationalization waves in Syria, Egypt, and Iraq drove Gulf and Levantine wealth toward Beirut’s secretive banking sector. The 1956 Banking Secrecy Law, championed by parliamentarian Raymond Eddé who declared his ambition to make Lebanon “the bank of the Arab world,” anchored this model. Yet fragility was exposed by the spectacular collapse of Intra Bank on October 14, 1966—then the country’s largest lender holding fifteen percent of total deposits—which sent shockwaves through the exchange. The civil war progressively strangled the market until the exchange suspended operations in 1983. Revival came with Rafik Hariri’s reconstruction: trading resumed November 22, 1996, listing just a handful of securities with Solidere shares quickly dominant. Hicham Safieddine’s Banking on the State (Stanford, 2019) situates these developments within a longer arc of state–finance entanglement shaped more by oligarchic banking interests than market forces. The assassination of Hariri in 2005 triggered a sharp sell-off; the sovereign default of March 2020 and the port explosion four months later plunged the exchange into existential crisis.

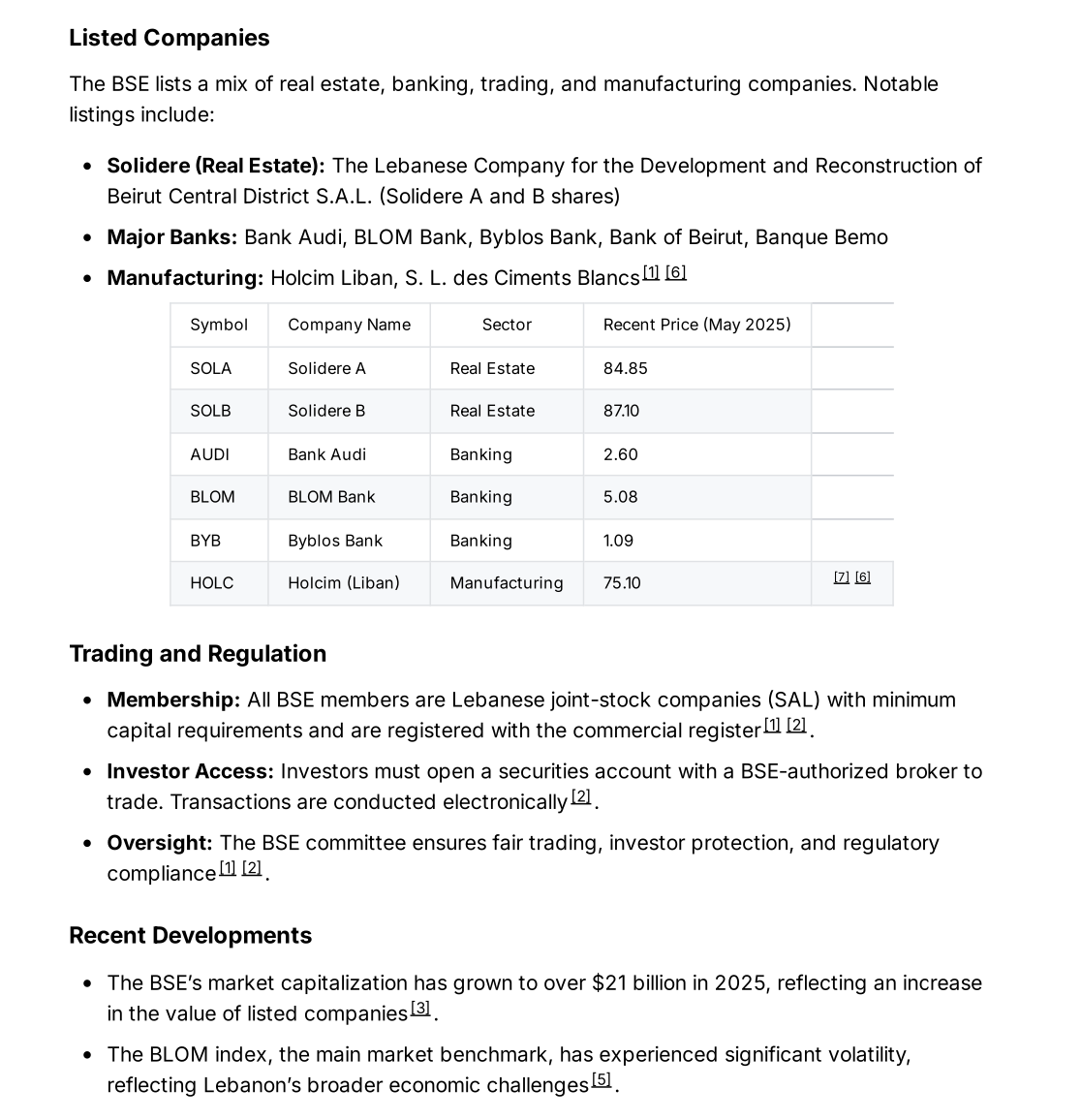

The securities traded on the Beirut Stock Exchange mirror the structure and vulnerabilities of the Lebanese economy. In its earliest decades under the French Mandate, the bourse dealt principally in gold and foreign exchange, reflecting Beirut’s role as a currency-arbitrage center linking the franc zone to regional markets. By the 1930s, equity shares of mixed Franco-Lebanese joint-stock companies—concessionary utilities, transport firms, banking houses—joined listings, quoted simultaneously in Paris. The postwar golden age saw banking stocks become marquee instruments. Lebanon’s 1956 Banking Secrecy Law attracted Gulf petrodollars; bank numbers surged from nine in 1945 to eighty-five by 1960, and their shares formed the BSE’s equity backbone. After the civil war hiatus, the reconstituted exchange was dominated by Solidere, the Société Libanaise pour le Développement et la Reconstruction de Beyrouth. Created in 1994 with 36,000 shareholders—former property owners compensated with Class A shares and new investors holding Class B shares—Solidere’s share price rose from five dollars in early 2004 to thirty-nine dollars at the September 2008 peak, routinely accounting for the vast majority of BSE volume. Its Global Depositary Receipts also traded on the London Stock Exchange. Beyond equities, the BSE listed Lebanese government Eurobonds—dollar-denominated sovereign debt central to the country’s fiscal architecture. Twenty-one Eurobond issues were listed, part of outstanding stock exceeding thirty-one billion dollars. When Lebanon defaulted on a maturing Eurobond on March 9, 2020—the first sovereign default in the country’s history—the BLOM Bond Index collapsed and the debt market froze. The Lebanese pound’s devaluation from the long-maintained peg of 1,507.5 to rates exceeding 80,000 by 2023 devastated locally denominated instruments.