Shanghai Stock Exchange

Shanghai, China · Established 1866

This site requires authorization to access.

To request access, contact

william.goetzmann@yale.edu

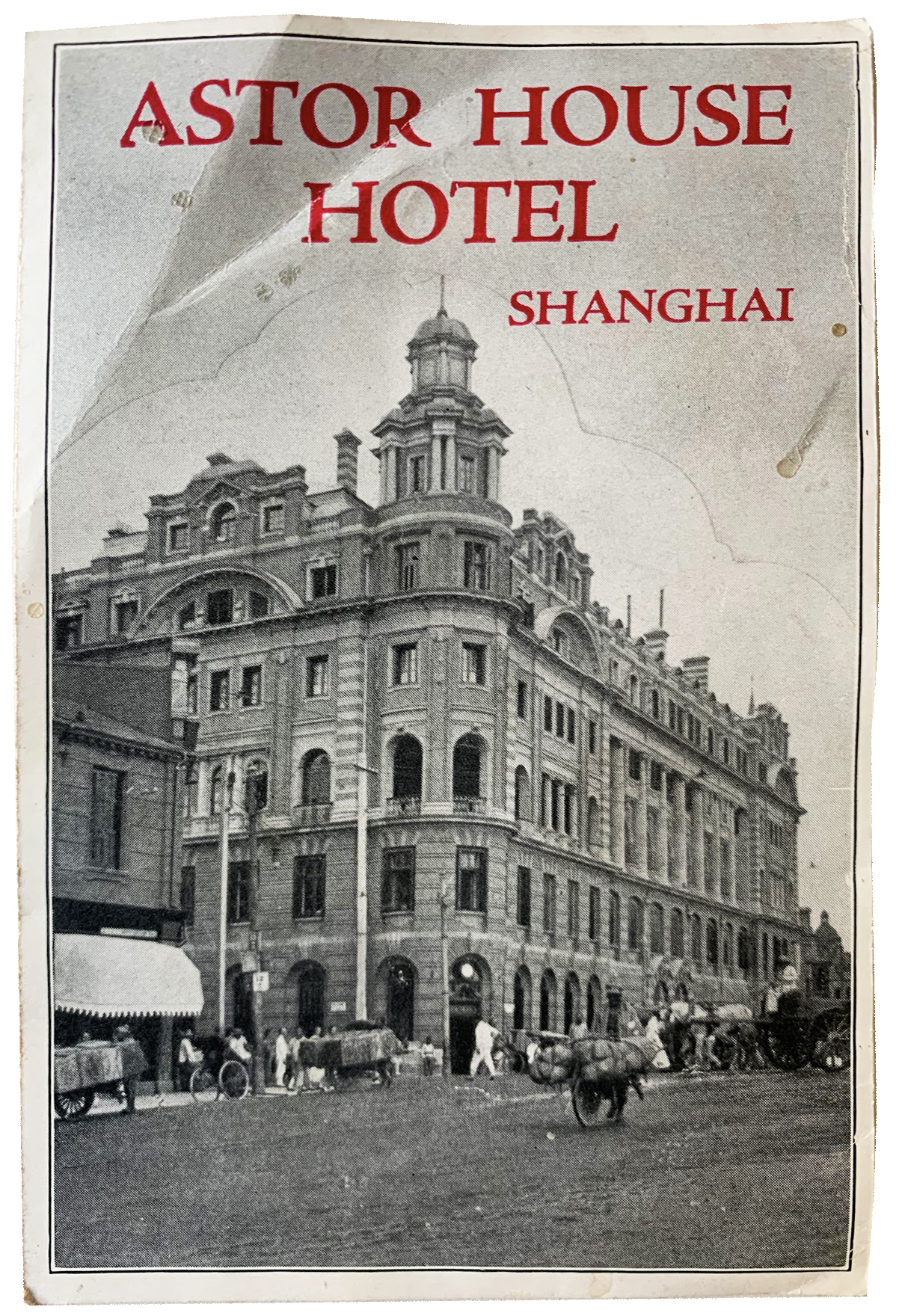

The architectural history of the Shanghai Stock Exchange spans three distinct structures across three centuries. The earliest formal securities trading in Shanghai took place not in a purpose-built exchange but in the offices of foreign brokerages scattered along the Bund and in the International Settlement. The Shanghai Sharebrokers’ Association, organized in 1891, operated from rented premises in the Settlement’s commercial district, as W.A. Thomas documented in Western Capitalism in China: A History of the Shanghai Stock Exchange (Ashgate, 2001). The first dedicated exchange building came in 1934, when the Chinese architect Lu Qianshou (Luke Him Sau, 1904–1991) designed the Shanghai Stock Exchange headquarters at 501 Jiujiang Road, near Nanjing Road and the People’s Square. Lu, one of the first Chinese students trained at the Architectural Association in London (1927–30), brought a modernist sensibility to the commission, as Edward Denison and Guang Yu Ren explored in Luke Him Sau, Architect: China’s Missing Modern (Wiley, 2014). The building was constructed by the Voh Kee Construction Company, also responsible for the nearby Park Hotel. The 1934 structure featured Art Deco elements characteristic of Shanghai’s Republican-era architecture, a style that blended Western modernism with Chinese ornamental detail. The building survives today in good condition and was renovated in 2015 by Stefano Boeri Architetti, who transformed its great hall into an open-air public passage and added a rooftop terrace. When the Shanghai Stock Exchange reopened on December 19, 1990, it initially operated from the Peacock Lounge of the Astor House Hotel (Pujiang Hotel) at 15 Huangpu Road—a Victorian-era landmark dating to 1846. The modern purpose-built headquarters, the Shanghai Securities Exchange Building at 528 Pudong South Road, was designed by WZMH Architects of Toronto and completed in 1997. The 26-story tower rises 109 meters and is crowned by a 70-meter flagpole. Its defining architectural gesture is an 18-story-high archway formed by two anchoring towers, bridged at the sixth floor by a 60-meter column-free trading hall that once accommodated 1,700 traders—the largest such floor in Asia. The building’s muscular steel exoskeleton, clad in silver aluminum and reflective glass, was conceived as a “gateway to the future,” symbolizing Shanghai’s emergence as a global financial capital. A 2014 interior renovation by OLI Architecture adapted the 3,600-square-meter trading floor for the digital age, introducing a glass-cylinder market oversight area, an IPO ceremony platform, and a specialty trading zone shaped in the Chinese character for “eight” (ba), evoking prosperity.

The decorative programs associated with Shanghai’s exchange buildings reflect the broader artistic heritage of the Bund’s commercial architecture. The most spectacular surviving interior near the exchange is the entrance hall of the former HSBC Building (No. 12, the Bund), designed by Palmer and Turner and completed in 1923. Its octagonal dome features elaborate mosaic murals depicting eight cities where HSBC maintained branches—London, Paris, Calcutta, Bangkok, Hong Kong, Shanghai, Tokyo, and New York—each accompanied by mythological figures and personifications of local rivers. The central dome portrays the Greek deities Demeter and Helios alongside zodiac signs, lions, and the figures of Apollo, Luna, and Fortuna. These mosaics were hidden under stucco in 1956 to protect them during the Cultural Revolution and rediscovered in 1997, as documented in Built Heritage (2022) in a study of the original paint finishes. The Customs House (No. 13, the Bund), also by Palmer and Turner (1927), contributes Doric columns and Greek Revival grandeur to the financial streetscape. The most prominent public artwork directly associated with the exchange is the Bund Bull, a bronze sculpture by Arturo Di Modica unveiled on May 15, 2010, on the Bund waterfront. Standing 3.2 meters high and 5.2 meters long, weighing 2.5 tons, the reddish-bronze bull was commissioned by Chinese officials as a companion to Di Modica’s famous Wall Street Charging Bull. The artist described it as “redder, younger and stronger,” leaning to the right rather than the left, with influences from both Western financial iconography and the Chinese zodiac’s Ox. Inside the modern SSE tower in Pudong, the 2014 OLI Architecture renovation introduced a glass-floored market oversight cylinder with illuminated LED news tickers displaying real-time market data, and conference rooms on the VIP floor house a museum documenting the SSE’s institutional history through archival photographs, stock certificates, and trading instruments. The Astor House Hotel, which served as the exchange’s home from 1990, was converted into the China Securities Museum in December 2018, displaying securities, bonds, and futures certificates dating from the Qing Dynasty through the modern reform era, preserving the material culture of Chinese financial markets within the very hall where the exchange was reborn.

The Shanghai Stock Exchange’s urban history is inseparable from the geography of the International Settlement and the Bund, the waterfront promenade along the western bank of the Huangpu River that served as the financial capital of East Asia from the 1860s through the 1930s. Following the Treaty of Nanking (1842), which forced open Shanghai as a treaty port, the British established a settlement along the river that merged with the American concession in 1863 to form the International Settlement, as Robert Bickers examined in Britain in China: Community, Culture and Colonialism 1900–1949 (Manchester University Press, 1999). The Bund’s dozens of Beaux-Arts, neoclassical, and Art Deco buildings housed the major banks and trading houses of Britain, France, the United States, Japan, Germany, and other nations—a concentration of financial power that scholars have compared to a “Wall Street of Asia.” The HSBC Building (1923), the Customs House (1927), the Bank of China Building (1937), and Sassoon House (the Peace Hotel) all stood within steps of the exchange’s offices. The French Concession lay to the south, the Chinese-administered old walled city beyond it, and the bustling Nanjing Road commercial corridor ran perpendicular to the river. Robert Bickers and Christian Henriot, in New Frontiers: Imperialism’s New Communities in East Asia, 1842–1953 (Manchester University Press, 2000), analyzed how this spatial arrangement concentrated financial, consular, and commercial functions along a single riverfront axis, creating an infrastructure of trust and proximity essential to securities trading. When the exchange reopened in 1990, it initially returned to the Bund, operating at the Astor House Hotel at the confluence of the Huangpu River and Suzhou Creek. But the decision to relocate to the Pudong New Area in 1997 represented a dramatic spatial reorientation. The Lujiazui Finance and Trade Zone, designated in 1990 directly across the river from the Bund, was transformed from agricultural and industrial land into a forest of supertall skyscrapers—the Oriental Pearl Tower (1994), the Jin Mao Building (420.5 meters, 1999), the Shanghai World Financial Center (494 meters, 2008), and the Shanghai Tower (632 meters, 2015). The SSE building at 528 Pudong South Road anchors the financial core of this district, surrounded by the offices of China’s major banks, securities firms, and the headquarters of the China Financial Futures Exchange. The juxtaposition of the historic Bund skyline and the Pudong towers across the river has become one of the defining urban images of twenty-first-century global finance.

Securities trading in Shanghai dates to the late 1860s. As William Goetzmann, Andrey Ukhov, and Ning Zhu documented in their Yale ICF working paper China and the World Financial Markets 1870–1930 (SSRN, 2001), a list of thirteen companies, including the Hong Kong and Shanghai Banking Corporation, appeared under a “Shares and Stocks” heading in the North-China Herald in June 1866. The International Settlement’s legal framework for joint-stock companies, its several banks, and the diversification interests of established trading houses provided conditions conducive to a share market. In 1891, foreign businessmen—primarily American, British, and French—established the Shanghai Sharebrokers’ Association, the first formal stock-trading organization in China. The Association registered in Hong Kong in 1904 under the Companies Ordinance and was renamed the Shanghai Stock Exchange, as W.A. Thomas traced in Western Capitalism in China (Ashgate, 2001). The exchange’s early decades were punctuated by the devastating rubber stock bubble of 1910, when 47 rubber plantation companies were listed and speculative fever drove prices to extraordinary heights before a sudden collapse. Jiajia Liu’s doctoral research at the Graduate Institute Geneva, Financial Capitalism on the Periphery (2021), demonstrated how Chinese investment leveraged through traditional qianzhuang (native banks) amplified the crash, triggering a cascade of qianzhuang bankruptcies and a systemic money-market crisis. In 1920 and 1921, Chinese-organized exchanges entered the field: the Shanghai Securities and Commodities Exchange and the Shanghai Chinese Merchant Exchange, founded by the Ningbo shipping magnate Yu Xiaqing. These merged with the older foreign exchange in 1929, and by the mid-1930s the combined Shanghai Stock Exchange had grown to become one of the largest in the Far East, with some 190 listed companies. The Japanese invasion of December 1941 forced permanent closure of the foreign exchange, as Liu documented in The Missing History of the Shanghai Stock Exchange, 1904–1941 (Amsterdam University Press, 2022). A brief postwar revival in 1946 ended when the People’s Liberation Army took Shanghai in 1949 and the new Communist government shuttered the exchange, liquidating and nationalizing its assets. For four decades, securities markets ceased to exist in mainland China. The reopening came on December 19, 1990, when Mayor Zhu Rongji presided over the inaugural ceremony in the Peacock Lounge of the Astor House Hotel—only the second stock exchange to reopen in a Communist state, after Budapest. Deng Xiaoping’s reform agenda and his 1992 Southern Tour further cemented Shanghai’s role as the engine of China’s market transformation. The SSE moved to its Pudong tower in 1997 and grew to become the world’s third-largest exchange by market capitalization.

The instruments traded on the Shanghai Stock Exchange evolved dramatically across its multiple incarnations. In the earliest period, beginning in 1866, the share list was dominated by banking stocks—particularly the Hong Kong and Shanghai Banking Corporation—alongside shares in shipping, insurance, dock, and utility companies such as the Shanghai Waterworks and the Shanghai Gas Company. As Thomas documented in Western Capitalism in China (Ashgate, 2001), by 1880 only the Hong Kong and Shanghai-based banks remained among the actively traded financial stocks. The Treaty of Shimonoseki (1895) permitted foreign factories in China, expanding the supply of manufacturing securities. The rubber boom beginning around 1909 transformed the market: by autumn 1910, forty-seven rubber plantation companies were listed, and rubber shares became, in Thomas’s phrase, the exchange’s “main dealing medium” through the 1920s and 1930s. Swan, Culbertson and Fritz calculated three weekly Shanghai indices in the 1930s tracking 23 Rubber Shares, 16 General Shares, and Internal Bonds—reflecting the three pillars of market activity. Chinese government bonds, mostly issued to fund railroad construction at a 5 percent coupon, traded alongside equities; yields remained below 6 percent until World War I but rose sharply as default and inflation risks mounted, with China defaulting on sterling loans in 1924–1925 (Goetzmann, Ukhov, and Zhu, SSRN, 2001). The Chinese-organized exchanges of the 1920s added futures contracts and commodities to the mix. Market capitalization peaked at approximately $1.7 billion in 1925 before declining to $235 million by the time of the Japanese closure in 1941. The modern Shanghai Stock Exchange, reopened in 1990, introduced a dual-share structure: A-shares denominated in renminbi and restricted to domestic investors, and B-shares denominated in U.S. dollars (later also available to domestic investors) for foreign participation. The exchange lists equities, government and corporate bonds, convertible bonds, T-bond repurchase agreements, exchange-traded funds, and securities investment funds. By the 2000s, the SSE had become one of the world’s largest equity markets. In July 2019, the SSE launched the Science and Technology Innovation Board (STAR Market), designed as China’s answer to Nasdaq, supporting technology companies with core innovations. The first twenty-five STAR Market listings raised 37 billion yuan collectively, and within a year the board had facilitated 200 IPOs raising $44 billion, establishing itself as a premier venue for Chinese technology “unicorns.”