Detroit Stock Exchange

Detroit, USA · Established 1907

This site requires authorization to access.

To request access, contact

william.goetzmann@yale.edu

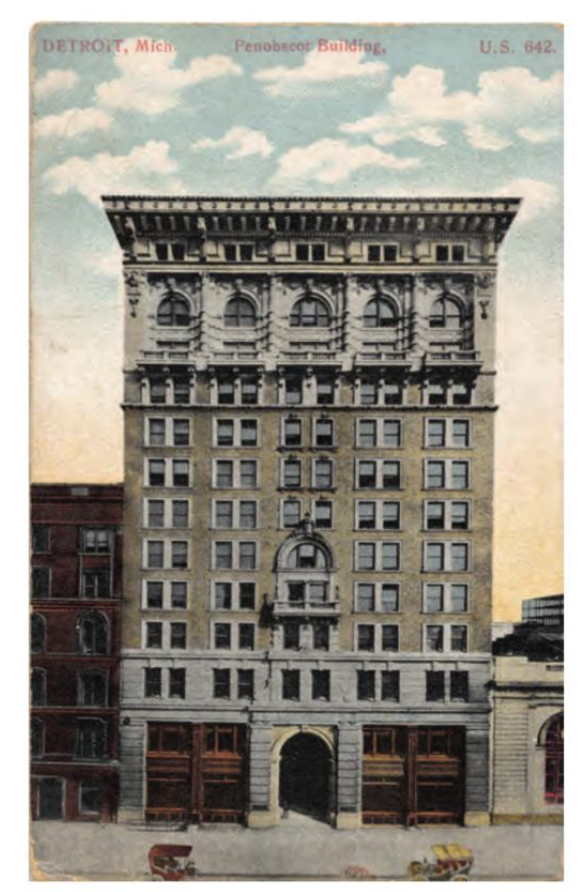

The Detroit Stock Exchange occupied two distinct architectural homes during its seven-decade existence. From 1907 the exchange moved through several interim spaces—beginning in a small room in the Moffatt Building, then migrating to the Dime Building, the former Detroit Journal Building on Shelby Street, and the Penobscot Annex—before commissioning a purpose-built headquarters. In 1930 the exchange hired the architectural firm of H. Augustus O’Dell and George F. Diehl to design a new building at the southwestern corner of Griswold and Larned Streets, in the heart of Detroit’s financial district. Ground was broken on June 2, 1930, the cornerstone placed on August 14, and the four-story structure—clad in cream-colored Mankato stone quarried in southern Minnesota—opened for business on March 2, 1931, at a cost of $600,000. Contemporary newspapers described the style as “Assyrian Revival,” though architectural historians now classify it as Art Deco, as documented in the Historic Detroit architectural database. The trading room offered twice the floor space of the Penobscot quarters, measuring fifty by seventy-five feet with twenty-three-foot ceilings; a mezzanine housed a spectators’ gallery, offices, and vaults. Just eight years after opening, however, the exchange defaulted on its mortgage—a casualty of the Great Depression’s devastating impact on Detroit’s economy—and was forced to retreat to the Penobscot Annex, where it would remain until closure in 1976. The 1931 building stood vacant for years before its demolition in 1983. Separately, the Greater Penobscot Building itself, designed by Wirt C. Rowland of Smith, Hinchman and Grylls and completed in 1928, soared forty-seven stories and 566 feet—at the time the eighth-tallest building in the world, as Kathryn Bishop Eckert details in Buildings of Michigan (Oxford University Press, 1993; revised edition, University of Virginia Press, 2012). Clad in Indiana limestone over a gray Mahogany granite base, the Penobscot rises for thirty stories before a series of setbacks culminating in a red neon beacon tower. Rowland’s design for the Penobscot, his second major skyscraper commission after the nearby Buhl Building, established the Art Deco vocabulary that he would refine in the celebrated Guardian Building completed the following year.

The decorative programs of the Detroit Stock Exchange’s 1931 headquarters featured the work of sculptor Emil Siebern (1888–1942) of New York, a protégé of John D. Rockefeller who had studied at Cooper Union and toured Italy and Greece on Rockefeller’s patronage. Siebern carved a monumental bas-relief panel above the main entrance depicting King Croesus of Lydia—the ancient monarch synonymous with wealth and the invention of coined money—flanked by a wrestling bull and bear, the traditional symbols of rising and falling markets. The iconographic choice of Croesus, as recorded in the Historic Detroit architectural database, connected Detroit’s modern financial marketplace to the deepest roots of monetary history. Additional carved stone panels depicted scenes from Detroit’s own commercial past: a Native American figure honoring the city’s pre-European era, a French fur trader representing the colonial period, and frontier settlers who braved the Michigan wilderness. When the building was demolished in 1983, preservationists rescued several of these Art Deco panels. The bull and bear sculpture survives today in the lobby of 150 West Jefferson Avenue, the office tower erected on the site, while other panels are displayed in the elevator lobbies of the law firm Miller Canfield. Siebern’s figure of Croesus, sadly, did not survive the demolition. The Penobscot Building, which housed the exchange for most of its existence, contains an even richer decorative program. Corrado Parducci (1900–1981), the Italian-American architectural sculptor who completed over 600 commissions in his sixty-year career, carved elaborate limestone reliefs for the building’s lower floors, as documented in Dale A. Carlson and Einar E. Kvaran’s Corrado Parducci: A Field Guide to Detroit’s Architectural Sculptor (2020). In tribute to the building’s patron, lumber baron Simon Murphy of Maine, Parducci created river-like motifs with floating logs alongside panels depicting Native Americans in elaborate headdresses hunting wolves and buffalo with bows and arrows—imagery that incorporated eagles and sun-worship symbols drawn from indigenous traditions. The metalwork throughout the lobby continued these Native American themes, while the grand four-story entrance arch on Griswold Street featured travertine carvings of exceptional quality, placing the exchange’s daily operations within a space that merged modernist Art Deco geometry with references to preindustrial North America.

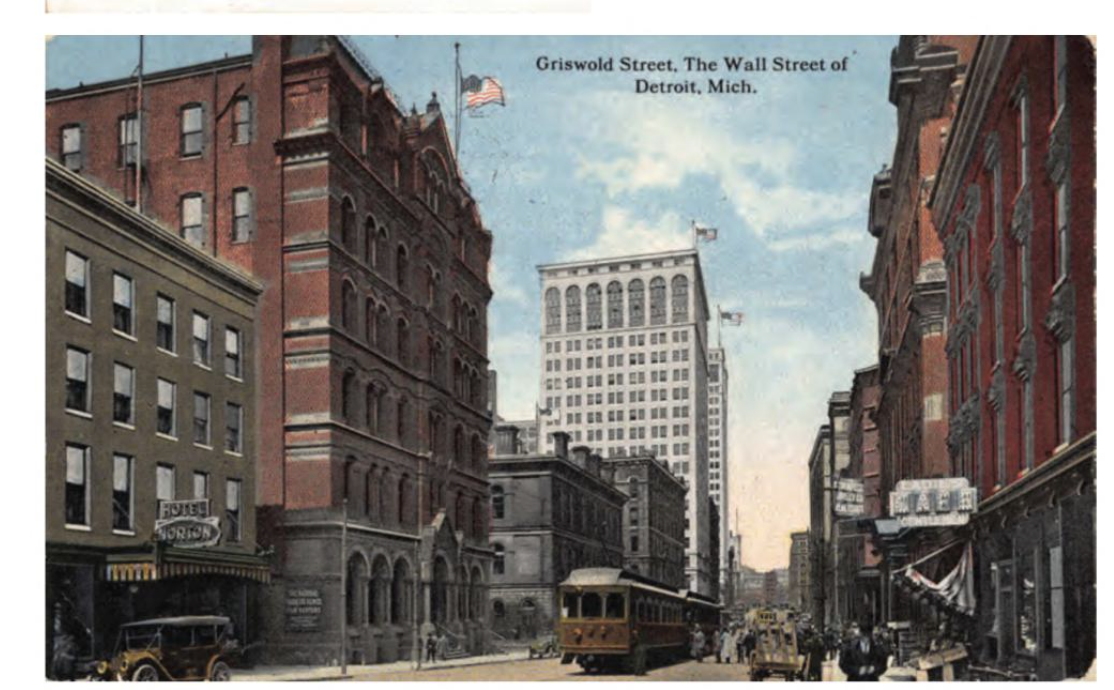

The Detroit Stock Exchange occupied a pivotal position within what historian Silas Farmer called in 1884 “the Wall Street of Detroit”—the dense financial corridor along Griswold Street between Jefferson Avenue and Congress Street. As documented in the Detroit Financial District’s National Register of Historic Places nomination (listed December 24, 2011), banks had clustered along Jefferson and Griswold since the 1830s, when the Bank of Michigan, the Farmer’s and Mechanic’s Bank, and the Michigan State Bank established premises there. By 1899, twenty of Detroit’s twenty-three banks operated on Griswold alone. The American Institute of Architects has described the district as “one of the city’s highest concentrations of quality commercial architecture,” and its thirty-three contributing properties were designed by a roster of nationally significant firms including D. H. Burnham and Company, Albert Kahn Associates, McKim Mead and White, and Smith Hinchman and Grylls. The exchange’s own 1931 building stood at Griswold and Larned, surrounded by institutions that both served and competed with it: the Guardian Building (Wirt C. Rowland, 1929), headquarters of the Union Trust Company, rose just blocks away, its Tiffany-tiled interior rivaling any banking hall in America; the Penobscot complex—where the exchange operated for most of its history—dominated the skyline; and the Dime Building, the Buhl Building, and the Ford Building filled out a streetscape that embodied the financial ambitions of America’s fourth-largest city. Detroit’s geographic advantages as a Great Lakes port and railway hub—connecting iron ore from Minnesota, copper from Michigan’s Upper Peninsula, lumber from the north woods, and coal from Appalachia—made it the natural site for an industrial stock exchange, as Steven Klepper argued in “The Evolution of the U.S. Automobile Industry and Detroit as Its Capital” (Carnegie Mellon University, 2002). The city’s population surged from 285,000 in 1900 to 1.57 million by 1930, and the financial district grew in tandem, its skyscrapers rising as vertical monuments to the capital flows that powered the automobile revolution.

The Detroit Stock Exchange was organized in 1907, opening in a small room in the back of the Moffatt Building on Griswold Street, as Steven Renaldi, an investment advisor and historian of the exchange, has recounted. The timing was deliberate: factories were proliferating across Detroit, and fledgling manufacturers—often short of cash—needed a local capital market where investors could purchase shares to finance the costly machinery that assembly-line production demanded. The exchange provided precisely this function, channeling local savings into the industrial enterprises that would make Detroit the Motor City. As Klepper documented in “Disagreements, Spinoffs, and the Evolution of Detroit as the Capital of the U.S. Automobile Industry” (Management Science, vol. 53, no. 4, 2007), over 200 automobile firms entered the industry in its first fifteen years, and the Detroit exchange facilitated capital formation for many of them. Buick, co-owned by William C. Durant, was listed on the Detroit Stock Exchange rather than the New York Stock Exchange, and in 1909 Henry Leland’s sale of Cadillac to Durant’s General Motors was reportedly the most significant transaction in the exchange’s early history. The exchange outgrew its Moffatt quarters, moving to the Dime Building and then to the former Detroit Journal Building before settling in the Penobscot Annex. By 1930, confident in Detroit’s industrial future, the exchange commissioned its own Art Deco headquarters, which opened March 2, 1931. But the Great Depression devastated the city: Michigan’s banking crisis of February 1933—triggered by the pending failure of the Guardian National Bank of Commerce and the First National Bank of Detroit, and deepened when Henry Ford refused to subordinate his deposits—led Governor William Comstock to declare an eight-day bank holiday that froze $1.5 billion in deposits and set off a national chain reaction, as documented in the Federal Reserve Bank of St. Louis’s FRASER archive. The exchange defaulted on its building’s mortgage around 1939 and retreated to the Penobscot Annex. It survived through the postwar decades as a regional marketplace, but the structural changes reshaping American securities markets proved fatal. On May 1, 1975—“May Day”—the SEC’s Rule 19b-3 abolished fixed-rate brokerage commissions, ending 183 years of the fixed-commission structure dating to the 1792 Buttonwood Agreement, as the SEC Historical Society’s gallery on market structure regulation documents. Regional exchanges had thrived partly because NYSE rules prohibited members from splitting commissions with nonmembers; negotiated rates eliminated this advantage. On May 12, 1976, the exchange’s members voted unanimously to dissolve, citing lack of interest and declining trading volume, and the Detroit Stock Exchange ceased operations on June 30, 1976—one of dozens of regional exchanges that closed in the consolidation wave that also claimed Honolulu (1977), Richmond (1972), and Colorado Springs (1966).

The Detroit Stock Exchange served as the primary regional marketplace for securities of the automobile manufacturers, parts suppliers, and industrial firms that defined Detroit’s economy. At its peak, Detroiters could trade shares in General Motors, Ford Motor Company, Chrysler Corporation, and Packard Motor Car Company alongside a diverse roster of regional enterprises: Kresge (the forerunner of Kmart), Detroit Edison (the city’s electric utility), Dow Chemical, Goebel Brewing, Kroger, Crowley Milner (a Detroit department store chain), Masco Corporation, Eureka Vacuum, and Sears Roebuck. The exchange’s founding purpose was to channel local capital into the machinery and plant expansion that Detroit’s manufacturers required. As Klepper explained in “The Organizing and Financing of Innovative Companies in the Evolution of the U.S. Automobile Industry” (in The Financing of Innovation, MIT Press, 2007), many early auto firms were not flush with cash, and selling stock to local investors through the Detroit exchange enabled them to acquire the expensive stamping presses, assembly equipment, and factory buildings that mass production demanded. The exchange thus functioned as a crucial intermediary in the capital formation process that transformed Detroit from a diversified manufacturing city into the world’s automobile capital. Trading was conducted on the open-outcry auction floor in the exchange’s various locations—the Moffatt Building, the Dime Building, the purpose-built 1931 headquarters, and finally the Penobscot Annex. Regional exchanges like Detroit also served an important structural role in the American securities market: they enabled commission-splitting between local brokers and out-of-town traders, circumventing NYSE rules that prohibited members from sharing commissions with nonmembers. This function, documented by the SEC Historical Society in its gallery on regional exchanges, sustained the Detroit exchange through the mid-twentieth century even as trading increasingly consolidated on national exchanges. When the SEC abolished fixed commissions on May Day 1975, the economic rationale for commission-splitting vanished, and with it the Detroit exchange’s remaining competitive advantage in a market increasingly dominated by the NYSE, the American Stock Exchange, and the nascent NASDAQ electronic system.